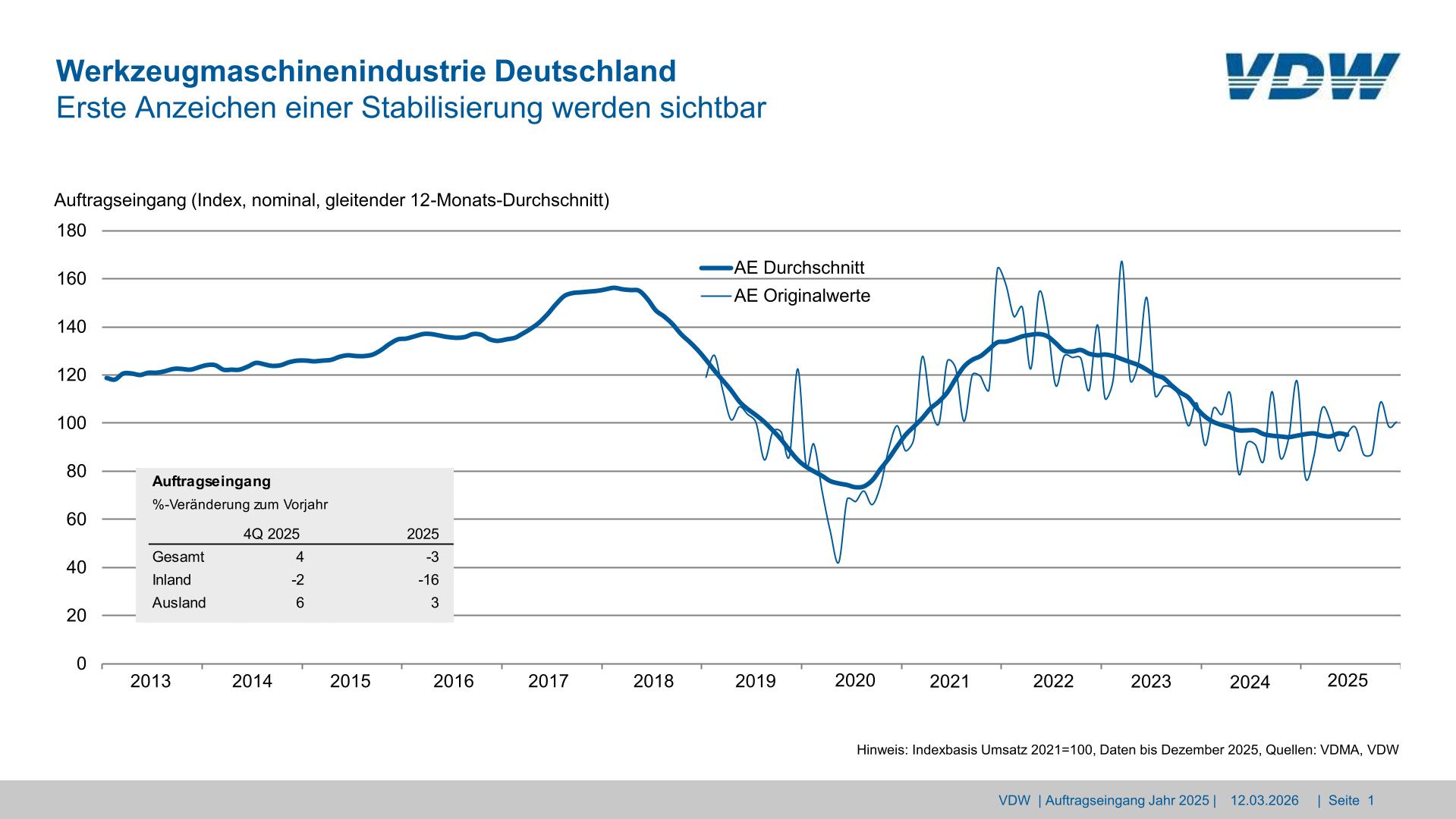

Frankfurt am Main, 18 March 2025 – After two years of noticeable reluctance to invest, the German machine tool industry is showing the first signs of stabilizing. Overall, however, incoming orders for 2025 remained slightly below that of the previous year. Orders declined by 3 percent – with considerably different developments at home and abroad. While international demand increased by 3 percent, new domestic orders plummeted 16 percent. The reluctance of many German industrial customers to invest reflects the difficult situation for key user industries, above all the automotive industry and its suppliers. A slight recovery was recorded by the end of the year, however: in the fourth quarter of 2025, the total number of new orders was up 4 percent on the previous year’s figure.

At the same time, there is an ongoing shift in global power relations when it comes to the machine tool industry. This has become particularly apparent with the rapid expansion of Chinese industry. Machine production (without parts and accessories) in the People’s Republic of China reached a new record level of approx. 30 billion euro in 2025. A development that sees China further cement its dominance in mechanical engineering worldwide. Germany, on the other hand, once again missed the 10-billion-euro mark for production volume. Reaching 9.4 billion euro, production only just exceeded the level of the 2020 and 2021 pandemic years. Overall, global production is still strongly focused on just a few countries. China, Germany and Japan together account for 58 percent of the machine tools produced worldwide, with 37 percent attributed to China, 12 percent to Germany and 10 percent to Japan. They are followed by the US and Italy with shares of 9 and 7 percent respectively.

Global market shifts

There are also noticeable shifts in international trade. The global export volume for machine tools reached around 41.4 billion euro in 2025, approx. 3 percent less than the previous year. Particularly striking here is the shift in positions at the top of the export rankings: China has outperformed Germany for the first time to become the world’s largest exporter. While German manufacturers delivered 10 percent less machinery abroad and recorded an export volume of 7 billion euro, Chinese suppliers increased their exports by 13 percent and achieved a new record of 8.6 billion euro. At the same time, China is by far the largest sales market for machine tools worldwide. Market volume grew by 5 percent in 2025 to reach 25.2 billion euro, with around 32 percent of worldwide consumption attributed to the People’s Republic of China. It is followed by the US with 11.1 billion euro and a market share of 14 percent. Germany achieved a share of 5.7 percent and lies only slightly ahead of India with 5.4 percent.

The VDW experts are expecting another resurgence in the second half of the year. Yet it is not the classic automotive or mechanical engineering industries, alongside arms and aviation, that are driving growth. The machine tool industry is currently gaining substantially more from the electronics and semiconductor industry, as well as their value chains. “This can be attributed to the rapid growth of digitalization, the AI boom and the global expansion of data centers,” explains Dr. Markus Heering, Managing Director of the VDW.

Business with the US also remains stable, despite ongoing commercial uncertainties. Investments are likely to further increase there in the coming months. When it comes to demand from China, prospects have improved slightly thanks to a strengthening of investment in future technologies and the classification of machine tools as critical core technology in the government’s new five-year plan. “These changing geopolitical conditions are leading to an even stronger realignment of economic partnerships. Shown, for example, in the free trade agreements planned with India and the Mercosur,” says Heering.