Euro zone accounting for significant proportion of machine tool orders at present

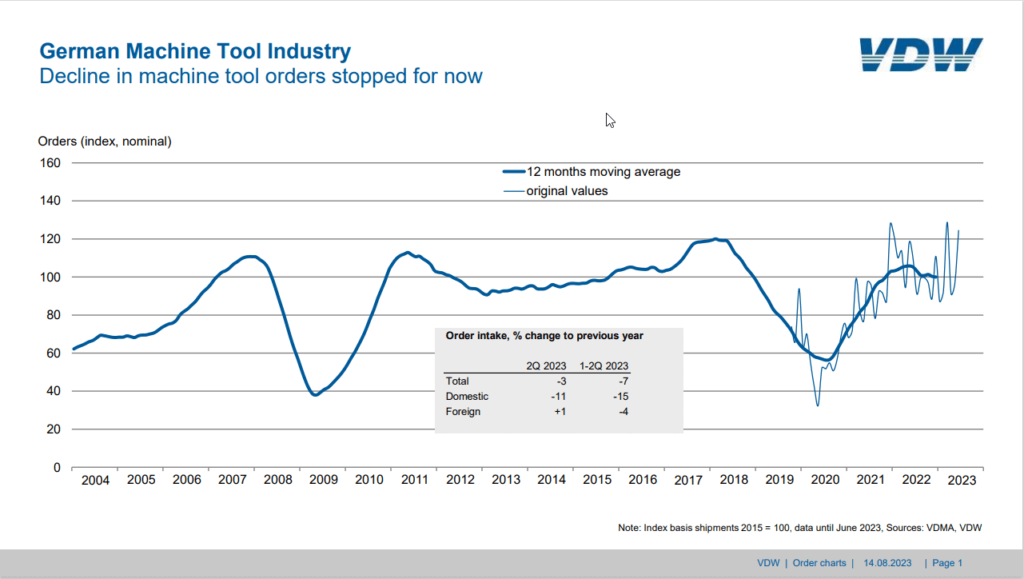

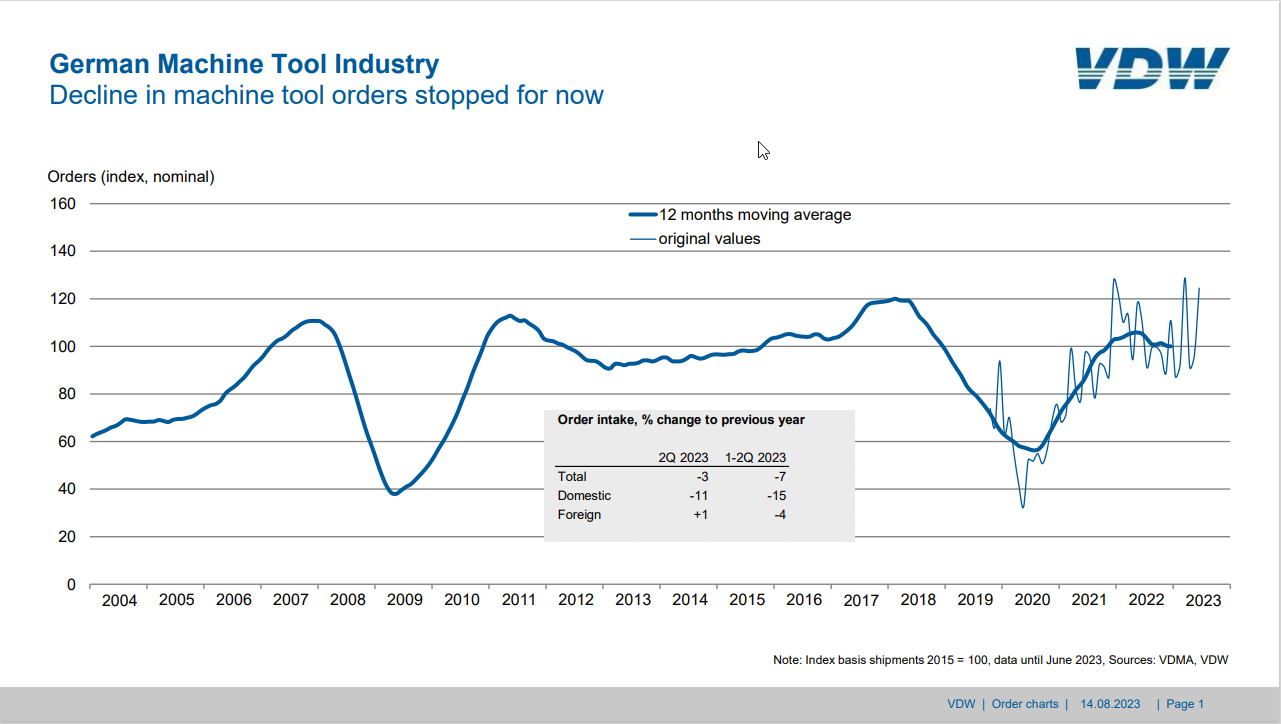

Orders received by the German machine tool industry in the second quarter of 2023 were 3 per cent down in nominal terms on the same period last year. Orders from Germany declined by 11 percent whereas those from abroad rose by 1 per cent. The level of orders fell by 7 percent overall in the first half of the year. Domestic orders were 15 percent down on last year, whereas orders from abroad were down by 4 percent. This represents a 13 percent drop in orders in real terms.

Orders received by the German machine tool industry in the second quarter of 2023 were 3 per cent down in nominal terms on the same period last year. Orders from Germany declined by 11 percent whereas those from abroad rose by 1 per cent. The level of orders fell by 7 percent overall in the first half of the year. Domestic orders were 15 percent down on last year, whereas orders from abroad were down by 4 percent. This represents a 13 percent drop in orders in real terms.

“There was a further surprising increase in order intake at the end of the second quarter, similar to March,” reports Dr. Wilfried Schäfer, Executive Director of the VDW (German Machine Tool Builders’ Association), Frankfurt am Main. The main impetus came from the euro countries in the second quarter. The increase in orders which materialized at the end of the second quarter applied to both machining and forming equipment. “We know from experience, of course, that the result of a single month does not signal a turnaround,” Schäfer continues. Rather, the fluctuations were attributable to project business, particularly to forming technology. In addition, orders from growth sectors such as e-mobility, wind power, aerospace and defense are boosting order intake levels. The conventional machine business, on the other hand, was somewhat weaker, as small and medium-sized customers are unsettled and are postponing investments. Credit-financed machine purchases are also becoming more challenging due to the rise in interest rates.

Sales remained steady at a high level. In nominal terms, it grew by 21 percent in the first half of the year, and by 13 percent in real terms. Capacity utilization rose again slightly in July this year, from 88.3 to 90.5 percent.

The order backlog is dropping relatively slowly. “Accordingly, the VDW forecast of 10 percent growth in production in the current year remains valid,” concludes Schäfer. Foreign markets continue to represent the principal driving force, and Asia is the only region with a positive balance sheet.

{kind=link}